If you’re a business owner, you may have heard of credit card surcharging but may need to understand all it entails. While passing a credit card fee on to customers might decrease sales, the cost of everything keeps rising, and you must manage your costs. Credit card fees can be the highest cost after labor for many merchants, especially small businesses.

Our goal for our Business Owners Guide to Surcharging is to make sense of surcharging and help you understand how it works and how it might benefit your business.

In this article, we’ll look at:

- What is surcharging?

- The pros and cons of surcharging

- How to set up surcharging: merchant best practices

- What to consider – whether to add surcharging or not

What is surcharging? A simple definition

- When you make a sale, and the consumer pays by credit card, you pay or absorb the fee. Absorbing credit card fees has historically been seen as a cost of doing business, but credit card fees can crush your business. A credit card surcharge is

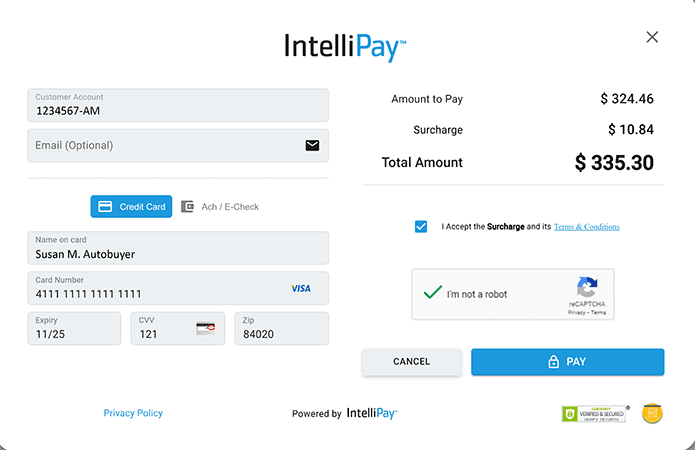

- a percentage fee added to the final transaction total when a consumer uses a credit card at checkout

- used only to offset the cost of credit card processing

- added to eligible Visa, Mastercard, Discover, and American Express Opt Blue credit card sales as an itemized line item at checkout

As a result, more and more business owners have shifted credit card processing fees to their customers to protect their margins. While you can raise prices to offset these costs, a surcharge allows the business to show customers the exact cost of using a credit card instead of other lower-cost payment methods like cash or debit cards.

The benefits and drawbacks of surcharging

When considering whether to pass credit card processing fees to your customers, you should also understand the pros and cons of surcharging.

What are the pros (benefits)?

Credit card surcharging offers two significant benefits:

Lower costs

If your business absorbs the processing fee on credit card sales, credit card processing is often the highest expense after labor. Consider this example. A small business has an average sale of $25 and is paying 2.9% + $0.30 on each credit card sale; that business is paying $1.03 in swipe fees alone. Now imagine if that business did 3,000 transactions, a $3,090 expense, which could be eliminated with surcharging.

Other convenient payment methods lower the final cost

When you show your customers, they have payment options that don’t incur high processing fees. You’ll enhance the customer experience when you help them see they get a lower final purchase price when using cash or debit cards.

The cons or drawbacks

Like most things in life and business, with surcharging, there are good and not-so-good things to consider.

Your sales could take a hit.

Conventional business wisdom suggests that a price increase typically leads to lower sales. With surcharging, you are not raising prices but shifting the cost to those who pay with a credit card. A survey of 2,500 consumers found that of consumers choosing not to pay the surcharge, 71% defaulted to cash. Generation Z cardholders used debit cards 72% of the time “as have 53% of millennial cardholders and 51% of bridge millennial cardholders.”

The same survey found that eighty-five percent who faced surcharges agreed to pay them.

If merchants in your industry include a credit card surcharge on sales, you would likely see only the cost-benefit. However, if your industry and competition absorb credit card processing fees, adding a surcharge to your customers could reduce your competitiveness.

It can impact customer’s perception of your business

Customers may prefer to avoid having to pay an extra fee to be able to pay with a credit card.

It only works for credit cards

Surcharging is only for credit card transactions. Debit and prepaid card transactions cannot be surcharged.

It can complicate your accounting

One reason why adding surcharges increases accounting complexity is that surcharges don’t show up on statements. So, you or your accountant would need to review each card transaction to see which has a surcharge. Another is processing fees range anywhere from 1.3% to 3.5%.

Best practices for getting started with credit card surcharges

If you want to proceed after considering the pros and cons of surcharging, you need to ensure your business complies with card brands (Visa, etc.) rules and all laws and regulations.

Checking your local laws and regulations

Currently, two states, Massachusetts and Connecticut, and the territory of Puerto Rico, ban surcharging; however, other states may impose additional requirements. For example, New Jersey and New York limit surcharging to the cost of processing. New York also requires merchants to “clearly and conspicuously post the total price for using a credit card” in such a transaction, including the surcharge. Therefore, we recommend checking with a local business accountant, tax specialist or lawyer to ensure compliance prior to implementing a surcharge. Please see our complete surcharging guide here.

Register with acquire/payment processor

Before April 15, 2023, to surcharge, your business had to register with the card brands, such as Visa and Mastercard. That requirement has been changed to notifying your acquirer/payment processor 30 days before introducing surcharging.

Must inform customers of surcharges

If you’re a brick-and-mortar business, you must post signage at your store entrance and at the point of sale that using a credit card will incur a fee and what the fee is. Some states have additional requirements, New York and Maine.

Online businesses must provide a surcharge notification before checkout and have a place where customers agree to accept the charge. On all receipts, in-person or online, the surcharge must be a line item and include the fee.

Understand the maximum allowable surcharge

The surcharge must be, at most, your cost of processing the payment or 3% of the transaction amount.

Should your business add surcharges?

Since the pandemic, surcharging has become far more widespread. More merchants have introduced surcharging due to inflation, continuing challenging economic conditions and by the broader drive to support local businesses.

Is surcharging right for you? That depends on your business, industry, and other local factors. Consider what your competitors are doing, the impact adding a fee might have on your customers, and the savings you would see by surcharging. Recent experience has shown while adding a credit card surcharge might lead to losing some customers, the cost savings more than offset the potential loss of customers.