Contents

- The Anatomy of a Merchant Statement: A Merchant’s Guide to Transparency

- Quick Answer: How to Audit Your Statement in 60 Seconds

- 1. Identify the “Hidden Three”: Common Statement Red Flags

- 2. The 5-Step Statement Audit Workflow

- 3. 2026 Regulatory Alert: Nacha & FTC Compliance

- 4. Frequently Asked Questions (FAQs)

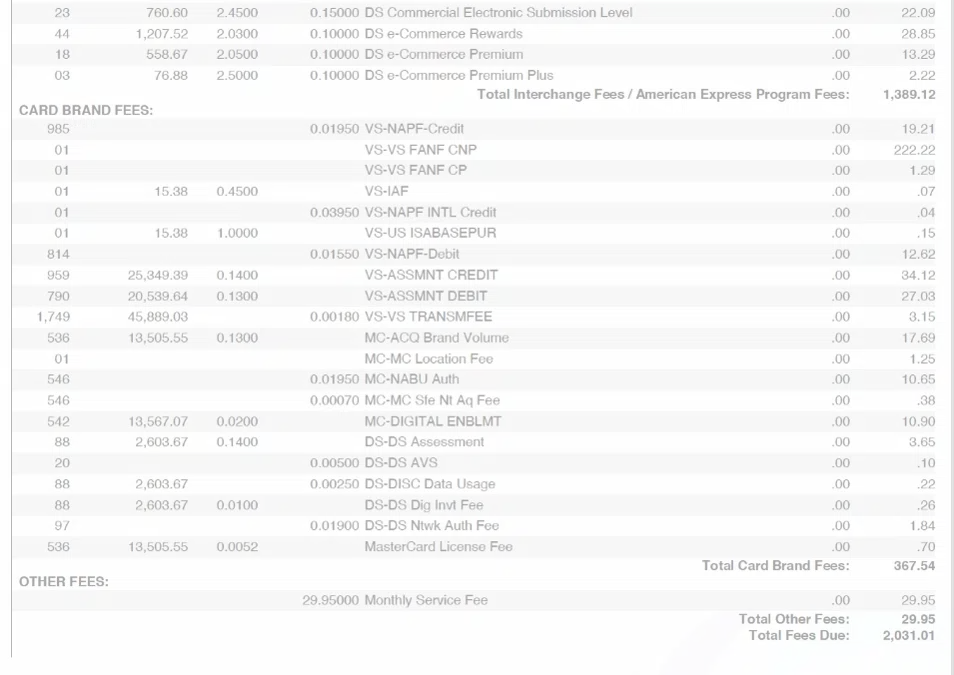

The Anatomy of a Merchant Statement: A Merchant’s Guide to Transparency

By Dale Erling | 15+ Year Payments Strategist | Reviewed by Jess Hunt, Risk Manager Last Updated: January 9, 2026 | 5 Minute Read

Quick Answer: How to Audit Your Statement in 60 Seconds

To quickly audit a merchant statement, calculate your Effective Rate by dividing your Total Fees by your Total Processing Volume. If your rate for a standard retail or auto shop exceeds 3.5%, you are likely paying “junk fees” such as PCI Non-Compliance ($19.95+), Statement Fees ($10+), or inflated Gateway charges ($25+).

1. Identify the “Hidden Three”: Common Statement Red Flags

In 2026, junk fees are often disguised under generic labels to avoid scrutiny from the FTC Junk Fee Rule. Underwriters at your processor are watching how you manage these costs; ignoring them can signal a lack of oversight that negatively impacts your internal “Risk Score”.

PCI Non-Compliance Fee: Typically $19.95 to $99.00 per month. This is a penalty fee that can be eliminated immediately by completing a simple security self-assessment (SAQ).

Miscellaneous/Regulatory Optimization Fees: Often $5–$15. These are frequently pure processor markups with no corresponding service or actual regulatory requirement.

Batch Header/Settlement Fees: While a standard batch fee is roughly $0.10–$0.30, unscrupulous processors add “monthly settlement” fees of $10–$25 on top of daily charges.

2. The 5-Step Statement Audit Workflow

Use this structured process to verify you aren’t overpaying. Merchants who perform monthly audits can often reduce costs by 20%–30%.

Calculate Your Effective Rate: (Total Fees ÷ Total Gross Volume) x 100.

Audit Your Risk Indicators: Monitor your Chargeback Ratio and Average Ticket Size. In 2026, processors use these to build your profile; a ratio over 1% or erratic ticket sizes can lead to automated account freezes.

Verify Your Pricing Model: Ensure you are on Interchange-Plus pricing. If your statement shows “Qualified” vs “Non-Qualified” tiers, you are on a Tiered Model that hides significant markups.

Reconcile Bank Deposits: Match the “Net Deposit” on your statement to your actual bank account credits to catch “hidden” reserve fund deductions.

Check for Equipment Leases: Audit for “Service Fees” that equal the cost of a terminal over time. A “free” terminal often costs over $2,000 in hidden rate markups over three years.

3. 2026 Regulatory Alert: Nacha & FTC Compliance

Your statement health is now influenced by two major 2026 shifts:

Nacha Fraud Monitoring (Effective March 2026): New rules require businesses using ACH to implement risk-based processes to identify fraudulent entries. You may see new “Account Validation” or “Identity Verification” line items as a result.

Corporate Transparency Act (CTA): While 2025 saw some scope reductions, many foreign-formed entities registered in the U.S. still face strict Beneficial Ownership Information (BOI) reporting. Processors monitor this as part of their KYC (Know Your Customer) protocols, and non-compliance can lead to processing holds.

4. Frequently Asked Questions (FAQs)

Q: Why does my statement show ‘Non-Qualified’ transactions? A: This happens in Tiered Pricing when a “premium” card (like a rewards card) is used. The processor “downgrades” the transaction to a higher rate to increase their margin.

Q: Can I negotiate my processor’s markup? A: Yes. While Interchange Fees (paid to banks) and Assessment Fees (paid to Visa/Mastercard) are non-negotiable, the Processor Markup is entirely negotiable.

Q: What is a “Reserve,” and why does it appear on my statement? A: A reserve is a portion of your funds held by the processor to mitigate risk from chargebacks. High-risk industries or new businesses often see a “Rolling Reserve” deducted from their daily deposits.

General Financial Disclaimer: The information provided in this guide is for informational purposes only and does not constitute financial, legal, or professional accounting advice. While every effort is made to ensure accuracy, payment processing rates and industry regulations—including the FTC Rule on Deceptive Fees (2025) and 2026 Nacha Rules—are subject to rapid change. Seek independent professional guidance before making financial decisions.