Convenience Fee – Protecting Merchant Margins

Consumers want to choose how to pay and with whatever card they want. All that convenience comes at an expense to merchants. Every time you accept a card, there are fees. Each card transaction includes assessment, interchange, and transaction fees. One way to combat ever-increasing processing fees is to add a convenience fee to each sale.

What is a convenience fee?

A convenience fee. is charged when a customer uses a credit card to make purchases rather than using cash or checks. It’s usually added on top of the purchase price and is typically between 1% and 3% . A merchant can charge a customer a convenience fee for paying in a manner that’s not customary for the business (for example, online or over the phone).

- A convenience fee is different than a service fee or surcharge.

- A service fee is only for certain types of education and government merchants.

- A surcharge is a fee to cover credit card fees associated with a processing a transaction.

Are convenience fess legal in all fifty States?

Yes, credit card convenience fees are legal in all fifty states when a customer uses a payment form that isn’t customary to the business.

Can convenience fees be charged for all credit card transactions?

Yes, provided the customer has the option of paying with cash or check before completing the transaction. Because convenience fees incentivize using alternate payment channels to offset or avoid the costs associated with card processing, merchants should make it clear that the fee isn’t an additional profit center for them.

Can convenience fees be charged as a percentage of the transaction amount?

No, a convenience fee has to be a flat fee (say, $2 per transaction) rather than a percentage of the transaction amount (such as 2% of the total).

Can convenience fees be charged when the cardholder is using cash or a debit card?

A convenience fee cannot be charged when a customer chooses to pay with cash. However the fee can be added to all debit card transactions. If the cardholder has been given the option to choose cash or check.

Can convenience fees be charged for online purchases?

Yes. If online purchases are not a customary way to receive payment, you can charge a convenience fee. If your business only makes sales online, you cannot add a convenience fee.

How can adding a convenience fee lower card processing costs?

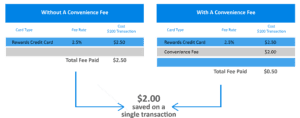

Convenience fees can be used to offset the costs of processing a card transaction, lowering the overall cost of payment processing. In the example below, the merchant used a $2 convenience fee to lower the $100 credit card transaction cost.

Convenience Fee Impact on Margin – $100 Purchase Example

The Need to Communicate

There is no question that merchants can boost their margins by adding a convenience fee.

At this point, you might be thinking, won’t adding a convenience fee alienate customers, or reduce sales? The answer is probably not. Consumers prefer the convenience and will pay for it. Research by Epsilon, a market research firm surveyed Amazon customers and found that 60% of consumers cite free shipping, and 52% cite convenience as a reason for buying on Amazon.

Further, government, education, utilities, and online ticketing organizations have acclimated consumers to paying fees for using convenient alternative methods to pay.

Finally, merchants in other industries use fees to cover processing costs. Gas stations have cash and credit prices. Insurance companies charge a fee for recurring payments that varies by payment type. And purchasing your weekly groceries online costs more than shopping yourself. At the end of the day, you and I are still being charged more for the convenience of shopping remotely and using plastic.

Consumers Don’t Understand the Cost of Credit

As mentioned earlier consumers have no idea that the merchant pays fees for each transaction; and a small number of consumers will push back on being charged a fee. Before adding a the fee, communication with your customers is essential. Credit rules require that consumers need to be made aware that a fee will be charged at the point of sale and that free payment options are available, such as paying in-person or by mail.

The ways to reach out to consumers vary by business and industry, whether it’s a notification in an invoice, a mention on the website, newsletter, etc. the better you can relate your story the less friction you will experience at the point-of-sale.

Convenience Fee Rules and Regulations

Card brands (Visa, Mastercard, etc.) or card association rules permit merchants to charge convenience fees under conditions. Merchants need to comply with these rules to remain within the terms of their merchant agreement to continue to accept credit cards. Here are the key points:

- Convenience fees are permitted when the payment channel is an alternative payment method to the method typically used by the merchant or industry.

- A convenience fee is a flat fee, and that is charged equally across all debit or credit card transactions no matter how large the transaction or the brand of the card used.

- Consumers must have notice that a convenience fee will be charged and agree to it before the transaction groceries.

- Cannot be charged on card-present transactions

- For government or educational institutions, a convenience fee is called a service fee and is limited to a select group of MCCs or merchants’ numbers.

Although convenience fees are not illegal nationally, local laws may affect how a merchant can add a convenience fee to their credit and debit card transactions.

Alternative Strategy

Wary your customer won’t like a convenience fee? Another way to offset processing costs is to set a minimum transaction amount for credit card transactions. The minimum transaction amount can be no more than a $10. While you are not required to disclose minimum purchases, we recommend it.

How can IntelliPay streamline payment processing and time spent with payments?

For merchants, taking card payments is a fact of life; absorbing all of the processing costs doesn’t have to be. IntelliPay helps merchants with transparent and affordable credit card processing fees in various ways. Unlike many other merchant service providers, we understand what its like to run a small business. So, We ensure there are no junk fees associated with our services. We are committed to providing clear, transparent interchange plus pricing, so there are no surprises when it comes to your payment processing expenses.

In addition to transparent pricing and consumer fee-based options, like convenience fees, we are an all-in-one payment gateway and payment processing solution for online and in-person payments with modern interfaces that simplify payments for your customers, encouraging online adoption. Easy online payments also reduce late or missed payments and the time spent by staff tracking them down.

Our cloud-based management console makes access to our advanced reporting and management features available anywhere you are while simplifying reconciliations and time spent managing payments.

Finally, the IntelliPay suite makes it easy to set up and customize a program to the needs of your business. You pay for what you need, nothing more. For more information, or to schedule a demo, contact IntelliPay at 855-872-6632 option 3 or click here.