Credit Card Processing Fees and Merchant Margins

In this two part series, we dive into credit card processing fees. In part one, we dive into what goes into the credit card processing fees you pay, and how to calculate your total processing cost. In part two, we look at actionable ways merchants can offset credit card processing fees.

Part 1

If you currently accept credit cards for payment, and who isn’t, rising credit card fees are eating into your budget! The major card brands (Visa, MasterCard, etc.) “review” their fees twice, usually in April and October. Unless you’re a major eCommerce company or supermarket chain, these twice-annual reviews can and do often equate to changes in interchanges rates and associated fees.

Breaking Down the Fees

The major card brands have two major classes of fees, interchange and assessment. Therefore, a high-level understanding of how each fee type works is essential in calculating what credit card transactions are costing you.

Interchange fees are the non-negotiable transaction fees that the merchant’s bank account must pay whenever a customer uses a credit/debit card to make a purchase.

Assessment fees are non-negotiable and charged on your total monthly sales for each credit card brand and is paid entirely to the credit brand (Visa, Mastercard, etc.). nt.

Like interchange fees, the card brands review assessment fees twice a year and are subject to change-read increases.

The combination of interchange and assessment fees is also known as “swipe fees” and makes up 80% to 90% of the transaction cost.

It is worth noting that interchange fees and assessment fees are the same for all merchants and payment processors regardless of size or credit card volume, which brings us to markup.

Markup

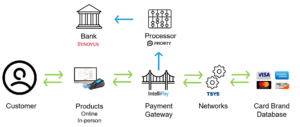

Markup fees are charged by third parties involved in processing credit or debit card payments on behalf of a merchant. The diagram below illustrates the flow and number of parties involved in processing a credit card transaction.

Markup fees make up 20% to 25% of the transaction and vary from processor to processor and depend on various factors such as pricing model, transaction amount, gateway, services used, etc.

Internal Costs are hidden costs or costs you incur to process payments. Examples are the purchase or rental costs of credit card terminals, internet and data connections, compliance requirements, software, supplies, IT support, accounting, and other related expenses that vary by location industry and business model. In summary, the low rate your processor provided you upfront is only a part of the total cost of accepting credit cards for payment.

A word about cash back and mileage points these perks are paid by merchants through higher interchange and other fees. Credit card processing fees have increased by over 200% in the past ten years, primarily due to the overwhelming popularity of premium reward credit cards – cards offering cash back or points toward free trips and other perks. Recent research estimated that over 92% of all credit transactions are made on a rewards card, and card issuers continually add new rewards levels with more lavish perks to remain competitive.

Understanding your Net Effective Rate

To understand how credit card processing costs impact your bottom line, we need to analyze your payment mix. The payment mix, for our purposes, is defined as the payment types (credit, debit, ACH) and the channels (in-person, over-the-phone, online) used to make the payment.

For example, if premium or reward credit cards were 20% of your payment type mix five years ago, and now they are 90%, your payment processing costs have dramatically changed. Why? Because the new premium credit cards have up to twice the fees of traditional non-premium reward credit cards and debit cards.

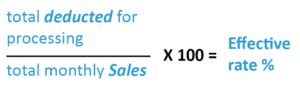

The first step to calculating your actual or total processing cost is determining what you are currently paying per transaction or industry vernacular your net effective rate. To find the effective rate, you first need to identify and then add up all the fees on your merchant statement.

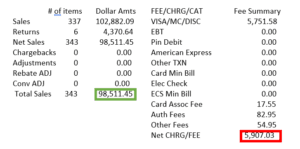

We’ll use the following merchant statement as an example:

In the example above, we have marked the total sales volume in green and the total fee in red. The formula for calculating the net effective rate is:

To complete this analysis, you’ll need to use the net effective rate formula once again. This time, substituting your internal costs for the total deducted for processing in the formula. Adding the two results will give you a more accurate view of your bottom line credit card payment processing costs.

Other Considerations

Now that you’ve got your head around the impact of accepting rewards credit card payments on your bottom line, there are other factors that you should be aware of that play into getting the best effective rates.

Low-risk or brick-and-mortar businesses with high transaction volumes will get the best effective rates on credit card processing. Why? More transactions lead to more revenue for the processor, with a higher percentage of in-person (card present) transactions means the risk of fraud is minimized.

As the percentage of online (card not present) payments increase, the greater the risk and the higher the effective rate. More about this in part 2 of this series.

If your business is with other businesses and most of your payments are on purchasing cards or business credit cards, look for a payment processor that processes payments with Level 2 and Level 3 credit card data. Level 2 and Level 3 transactions are processed with more data; the card brands see these transactions as more secure and less likely to be fraudulent or contain errors and qualify for lower credit card processing fees.

How can a company like IntelliPay help?

IntelliPay has over 100 years of combined payment industry experience working in a wide variety of industries and verticals. We help merchants develop an optimized payments strategy for their business, industry, and customers that goes far beyond an attractive, effective rate.

Beyond API integration into existing back-end systems that merely post payments as they occur, we work with merchants to develop solutions that automate payment flows, solve business challenges, and remove friction for consumers and staff. For more information, and a no-obligation consultation, contact sales.

Summary

Processing costs will continue to rise. Being educated to the real cost of credit cards helps merchants to accurately account for internal costs and take actionable steps to reduce them. Savvy merchants see beyond the teaser rates and marketing jargon, for solutions that actually improve margins, and simplify payment management.