Contents

- What are the Types of EMV Chip Cards?

- Quick Answer: EMV stands for Europay, Mastercard, and Visa—the three companies that created the global standard for chip-based payment cards that generate unique codes for each transaction, significantly reducing fraud.

- What Does EMV Stand For?

- Chip and PIN and Chip and Signature

- Understanding EMV Chip Cards and Their Growth

- How They Work

- The Rollout and Expansion

- Changes Since Introduction

- EMV Chip Cards and In-Person Transactions

- Global Adoption of EMV Technology

- Why EMV Technology Matters

- How do EMV Card Readers Work?

- What is Dipping?

- Benefits of EMV Technology

- What are the Costs of Accepting EMV Chip Cards?

- Can I Run an EMV Debit Card “as credit”?

- What’s the Difference Between EMV and NFC Technologies?

- How can you accept EMV Payments as a Business?

- How Does EMV Affect Card-Not-Present (CNP) Transactions?

- Here are some ways EMV technology has impacted CNP transactions:

- Are There Any Known Problems Accepting EMV Chip Cards?

- EMV Chip Cards and Card Cloning – Can EMV Cards be Cloned?

- FAQs

- About IntelliPay

What are the Types of EMV Chip Cards?

Quick Answer: EMV stands for Europay, Mastercard, and Visa—the three companies that created the global standard for chip-based payment cards that generate unique codes for each transaction, significantly reducing fraud.

EMV chip cards are payment cards with embedded microchips that create unique transaction codes for each purchase, making them nearly impossible to clone. Named after Europay, Mastercard, and Visa, these cards have become the global standard, used in over 90% of card-present transactions worldwide. They come in two main types: chip-and-PIN (requiring a PIN code) and chip-and-signature (requiring a signature), with chip-and-PIN being more secure.

What Does EMV Stand For?

EMV is an acronym that stands for Europay, Visa, and Mastercard. These are the three major financial companies that collaborated to create and implement this chip-based technology for credit and debit cards. EMV technology enhances transaction security through embedded microchips in cards, reducing the risk of fraud and counterfeit activities. This global standard has now become widely adopted in the payment industry, replacing the traditional magnetic stripe on the back of the card system.

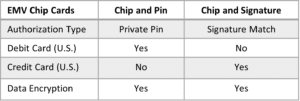

Chip and PIN and Chip and Signature

The EMV standard is the global standard for cards with integrated “computer” chips and the associated chip card authentication technology. While EMV technology is widely used and offers security benefits over magnetic stripe cards, consumers and businesses still need clarification about key components, such as the difference between ‘chip and PIN’ and ‘chip and signature.’

Chip and PIN vs. Chip and signature are the ways the cardholder authorizes a purchase. Chip and PIN card transactions, as the name implies, require the cardholder’s personal identification number (PIN) for authorization.

The PIN adds an extra layer of security, verifying that the cardholder is the card owner. The PIN must match the one associated with the card for the transaction to be approved. Chip and PIN cards are used in Europe and other parts of the world where PIN use is widespread.

In the U.S., chip and signature is common for credit cards. The cardholder signs at the time of sale, and the signature is compared with the signature on the back of the card or stored in the card issuer’s system. When the signature matches, the transaction is usually approved. In recent years, the adoption of signature cards has been declining in favor of PIN cards and other authentication methods.

Understanding EMV Chip Cards and Their Growth

EMV chip cards are a type of payment card equipped with a small computer chip. Named after the organizations that developed the technology—Europay, Mastercard, and Visa—these cards enhance security by creating a unique transaction code for every purchase.

EMV Chip

How They Work

- Chip Technology: Unlike traditional magnetic stripe cards, EMV chips store encrypted information, making them harder to clone or compromise.

- Authentication: During a transaction, the chip interacts with the card reader to confirm the card’s validity and generate a one-time code.

The Rollout and Expansion

The major shift to EMV chip cards in the United States occurred around 2015, following the EMV liability shift that encouraged merchants to adopt chip-enabled terminals. This addressed the critical need for more secure payment methods.

Changes Since Introduction

- Global Standardization: Most countries now widely use EMV technology, enhancing global payment security.

- Consumer and Business Adaptation: Over time, both consumers and businesses have become more familiar with the technology’s benefits, such as reduced fraud risk and increased transaction protection.

- Ongoing Confusion: Enhanced Education: As the technology matured, comprehensive resources and support systems have developed to help businesses and consumers understand and maximize the benefits of EMV security features.

Overall, EMV chip cards have fundamentally transformed payment security, demonstrating continual growth and global acceptance since their initial rollout.

EMV Chip Cards and In-Person Transactions

Here’s how an EMV chip card is used in an in-person purchase:

Insert or Tap Card: EMV chip cards must be inserted into a card reader chip side up or tapped against a card reader (if both the card and card reader are enabled for NFC contactless payments).

Enter PIN if Required: Some EMV chip cards require a PIN to authenticate the transaction. While there’s a trend toward more cards using PIN numbers to authenticate purchases rather than signatures, many cards still don’t require them.

Provide Signature if Required: While this isn’t as common as it used to be, some businesses still have policies that require customer signatures on card transactions for additional security against fraud.

Remove Card When Prompted: Most card readers or POS terminals will indicate when a transaction is complete, and the cardholder can safely remove their card.

By understanding both the authorization methods and the step-by-step process of using EMV chip cards, consumers can navigate in-person transactions with greater ease and confidence

Global Adoption of EMV Technology

EMV technology, a global standard for credit and debit card payments, has achieved substantial adoption worldwide. EMV technology has achieved near-universal adoption worldwide. According to recent data, the vast majority of payment cards globally are equipped with EMV chips, and EMV technology is used in over 90% of card-present transactions, highlighting its dominance in the payment industry. You can find the EMV standards here.

Why EMV Technology Matters

Enhanced Security: EMV chip cards offer superior security compared to traditional magnetic stripe cards. Each transaction generates a unique code, making it much more difficult for fraudsters to duplicate card information.

- Global Reach: The widespread use of EMV technology ensures that businesses worldwide are aligned with the most secure payment processes.

- Consumer Confidence: The robust security features of EMV cards provide consumers with greater confidence in the safety of their transactions.

Given these factors, understanding the workings of EMV technology is crucial for businesses aiming to protect their customers and reduce the risk of fraudulent transactions.

How do EMV Card Readers Work?

EMV card readers operate by extracting data from an embedded chip within the payment card. This process is fundamentally distinct from the traditional magnetic stripe (magstripe) cards, offering enhanced security through encrypted data transmission.

What is Dipping?

When it comes to EMV payments, dipping refers to a particular method of processing credit or debit cards equipped with a chip. Unlike the traditional swipe method, which involves sliding the card’s magnetic strip through a reader, dipping requires the card to be inserted into a chip-enabled terminal. Here’s how it works:

- Insertion: The customer inserts the card into the reader, chip side facing up and chip end going in first.

- Processing: The card remains in the terminal for the duration of the transaction. The chip technology helps ensure that the transaction is secure by generating a unique code for each transaction.

- Completion: Once the transaction is approved, the card can be removed from the terminal.

Dipping enhances the security of in-person card transactions by leveraging the encrypted data stored on the chip.

Benefits of EMV Technology

- Enhanced Security: The one-time code created by the EMV chip minimizes the risk of card fraud and data breaches.

- Reduced Card Cloning: Since the actual card number is never sent during the transaction, it’s extremely difficult for fraudsters to replicate.

- International Standard: EMV is widely accepted and standardized globally, ensuring compatibility across various markets and improving the overall security landscape for card transactions.

By understanding these steps, both businesses and consumers can appreciate how EMV technology not only facilitates smoother transactions but also significantly enhances the security of sensitive payment information.

What are the Costs of Accepting EMV Chip Cards?

There is no difference in cost to accept chip cards over magnetic stripe (Magstripe) cards. For example, the transaction cost is the same if your customer uses an EMV rewards card versus a Magstripe rewards card. Factors like the card type and where it is used are critical factors in the transaction cost. For example, a platinum business EMV card used for online purchases will have a higher transaction cost since business cards and online transactions have higher fraud risks.

However, for you as the merchant, there can be differences in the transaction costs you pay. If your customer uses a chip and PIN debit card, the interchange fees may be lower than if they used a chip and signature card. It is worth noting that debit cards processed on a card brand network can be more expensive than if the same card was processed on a PIN debit network.

Can I Run an EMV Debit Card “as credit”?

While there’s no difference in processing cost between chip cards and magstripe cards, there can still be some differences in costs. This is true when accepting debit cards.

Debit chip cards often have the option to skip PIN and run the card “as credit” instead. The cardholder can then sign for the transaction.

When debit cards are run “as credit,” the transaction will be routed through the card brand’s network and charged the debit interchange rates, not the often lower fees charged by PIN debit networks ( Star, NYCE, etc.).

When deciding how to accept cards and what equipment to purchase, we recommend that your equipment include a PIN pad for debit transactions. A PIN pad is significant because it allows customers to securely enter their PINs, enabling smooth debit transactions. This feature is particularly beneficial for merchants as it can lead to cost savings. Processing PIN debit cards is typically more economical than handling signature debit cards, offering a financial advantage that can enhance your bottom line. By incorporating a PIN pad, you’re not only improving transaction security but also optimizing your processing costs.

What’s the Difference Between EMV and NFC Technologies?

EMV Chip with NFC Symbol

NFC enables contactless, tap-to-pay functionality by wirelessly transmitting payment data between devices in very close proximity.

EMV generates a unique code for each transaction that is only readable by an EMV-enabled device during the transaction to protect data during transmission over card networks.

NFC payments leverage both technologies – NFC for the contactless interface and EMV for data security.

So, while not all EMV transactions use NFC, all NFC-based payments rely on the underlying EMV standard for secure data transmission and processing.

How can you accept EMV Payments as a Business?

Upgrade Your Card Reader

First, ensure that your card reader is equipped to handle EMV chip payments. Most modern card readers support EMV, but older POS systems might not. Double-check your equipment’s specifications or consult your provider to confirm compatibility.

Obtain the Right Hardware

If you currently don’t have a card reader capable of processing EMV payments, you’ll need to acquire one. Follow these steps:

Contact Your Payment Processor: Reach out to IntelliPay or your existing payment processor for recommendations on EMV-certified card readers.

Purchase a Compatible Reader: They might suggest specific models that are pre-certified for EMV payments, ensuring seamless integration with your current setup.

Set Up Your System

Once you’ve acquired the necessary hardware:

Install and Configure: Follow the manufacturer’s instructions to set up the card reader. This often involves connecting it to your POS system and configuring it according to your business needs.

Test Transactions: Conduct test transactions to ensure everything works smoothly. This step is crucial to prevent issues during actual customer interactions.

Train Your Staff

Make sure your staff knows how to operate the new card reader:

Teach EMV Payment Processes: Explain the steps involved in processing EMV payments. Typically, this includes inserting the card chip-first and waiting for authentication.

Highlight Security Features: EMV technology enhances transaction security, so emphasize the importance of this to your team.

Maintain Compliance

Stay updated on EMV compliance requirements to avoid potential security risks and fines. Regularly check for firmware updates for your card reader and consult with your payment processor on best practices.

Moving Forward

By upgrading your card reader, obtaining the right hardware, and choosing a reliable payment processor, you can start accepting EMV payments effortlessly. Proper setup and staff training will ensure a smooth transition, protecting both your business and your customers.

Following these steps will help ensure that your business is ready to accept EMV payments efficiently and securely

How Does EMV Affect Card-Not-Present (CNP) Transactions?

EMV technology was designed to secure card-present transactions, where the card is available at the point of sale. However, EMV chips are not used for online purchases, since online transactions are card-not-present (CNP) by nature, and thus don’t use this physical component of cards.

Here are some ways EMV technology has impacted CNP transactions:

Liability shift: With EMV, liability for fraudulent card-present transactions shifted from the issuer to the merchant if they don’t support chip technology. However, this liability shift does not apply to CNP transactions.

Rise of tokenization: To mitigate CNP fraud risk, tokenization (replacing card numbers with tokens) has become more prevalent for CNP transactions. Merchants and processors exchange meaningless tokens instead of real card data, reducing breach risks.

Dynamic authentication: Some issuers offer dynamic authentication like one-time passwords or biometrics for CNP transactions, adding an extra layer of security by requiring unique credentials for each transaction.

Fraud migration: As EMV made card-present fraud more difficult, fraudsters shifted focus to the more vulnerable CNP channel, increasing CNP fraud rates in countries that adopted EMV early.”

Are There Any Known Problems Accepting EMV Chip Cards?

At one time, EMV transactions were slower to process, but not anymore. However, some merchants still encounter occasional hiccups. Common issues reported include:

Terminals Not Requiring PINs

In certain instances, terminals fail to prompt for a PIN entry when an EMV debit card is inserted, despite this being a key security feature of the technology.

Lack of Cashback for Debit

Some terminals do not allow customers to get cash back when making a debit card purchase, limiting a convenient feature many consumers are accustomed to.

Unable to Skip PIN Entry

The reverse problem also occurs – terminals get stuck requiring PIN entry even for credit card transactions where a signature should be allowed instead.

EMV Chip Cards and Card Cloning – Can EMV Cards be Cloned?

Card cloning occurs when fraudsters extract the data stored on the chip and transfer it onto a counterfeit card with a magnetic stripe. The cloned card allows them to make fraudulent transactions at merchants that have not fully implemented EMV technology but still accept magnetic stripe cards.

The process typically involves:

Using a “shimmer” device installed on a card reader to illegally capture the EMV chip data when a legitimate card is inserted.

Transferring the stolen EMV data, including the iCVV (integrated circuit card verification value), onto the magnetic stripe of a counterfeit card.

Using the cloned magnetic stripe card at merchants that do not verify if the iCVV on the chip matches the CVV (card verification value) on the magnetic stripe. More on iCVV here

While EMV chips cannot be cloned, this bypass technique exploits the fact that many cards still have magnetic stripes as a fallback, and some issuers fail to validate the chip data properly. Stronger verification standards that check for mismatched chip and magnetic stripe data can help mitigate this fraud.

Learn more about iCVV security in our guide to Understanding iCVV’s Purpose in EMV Transactions

FAQs

What does EMV stand for?

EMV stands for Europay, Mastercard, and Visa—companies that developed secure, chip-based payment card standards.

What’s the difference between chip and PIN and chip and signature?

Chip and PIN cards require the cardholder to enter a PIN for transaction approval, while chip and signature cards require a signature. PIN-based transactions are more secure.

How do EMV chip cards help prevent fraud?

EMV cards generate a unique code for every transaction, making it much harder for criminals to clone cards or use stolen data.

Does accepting EMV chip cards cost more for businesses?

No, transaction costs are usually similar to magnetic stripe cards. However, EMV cards can reduce fraud liability, saving money long-term.

How can a merchant become EMV compliant?

Use EMV-certified card readers, ensure POS systems are updated, follow PCI-DSS rules, and train staff on secure transaction methods.

Can EMV chip cards be used for online purchases?

No, EMV chips are designed for physical (card-present) transactions. Online transactions use other security methods, such as tokenization and dynamic authentication.

What’s the difference between EMV and NFC?

EMV provides secure chip-based transaction codes. NFC enables contactless tap-to-pay, using EMV for data security and transmission.

What problems might occur when accepting EMV cards?

Occasional issues include terminal glitches, PIN prompts not appearing, or lack of cashback on debit purchases, often resolved by updating equipment or settings.

About IntelliPay

We help merchants optimize their payment processing through transparent interchange plus pricing, no junk fees, expert guidance, and reliable technology solutions. Our team combines deep industry knowledge with personalized service to ensure every client gets the best possible payment processing solution for their business.

The information provided on this page is for educational and informational purposes only. We make no representations or warranties regarding the completeness, accuracy, or security of this content, and all advice is provided “as is.”

Article last reviewed and updated: October 2025